Using a Lasting Power of Attorney

https://www.ellisbates.com/wp-content/uploads/2022/10/lasting-power-of-attorney-smaller-image.png 560 315 Jess Easby Jess Easby https://secure.gravatar.com/avatar/0e2a278e0eef1defdd7ee9d0ae7bb398?s=96&d=mm&r=g

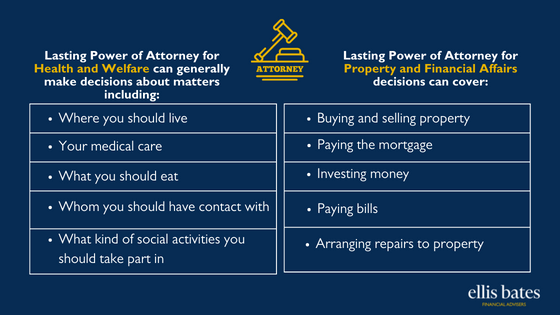

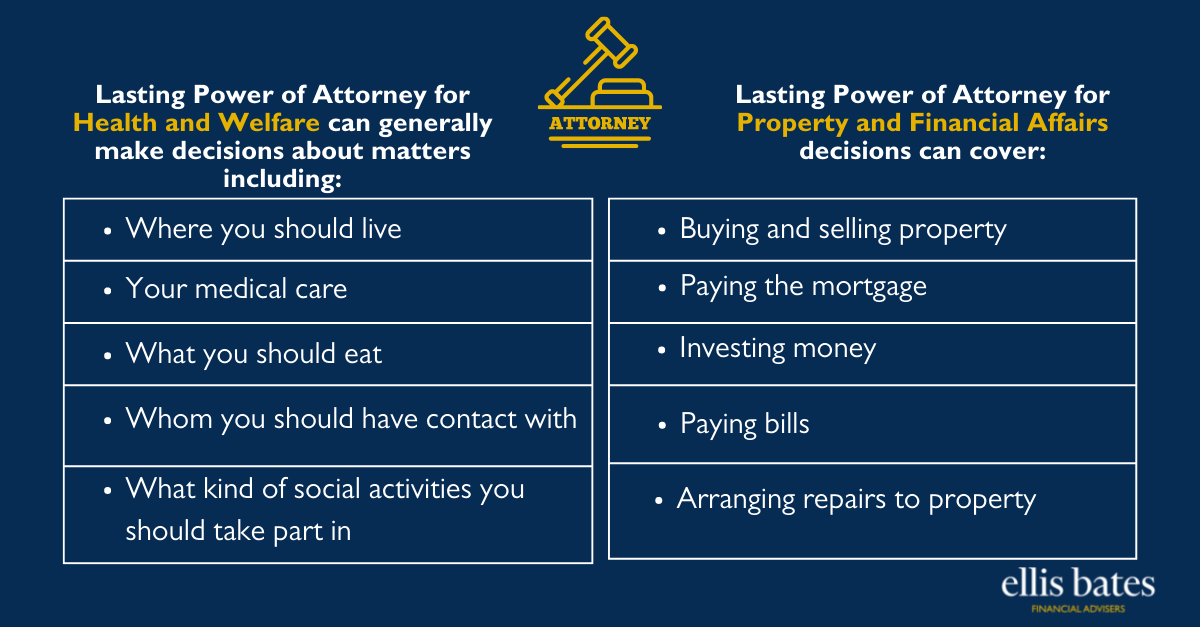

Lasting Power of Attorney for Health and Welfare can generally make decisions about matters including:

- Where you should live

- Your medical care

- What you should eat

- Whom you should have contact with

- What kind of social activities you should take part in

Lasting Power of Attorney for Property and Financial Affairs decisions can cover:

- Buying and selling property

- Paying the mortgage

- Investing money

- Paying bills

- Arranging repairs to property

Preserving your wealth and transferring it effectively.

Preserving your wealth and transferring it effectively.

Making decisions on your behalf during your lifetime

Making decisions on your behalf during your lifetime