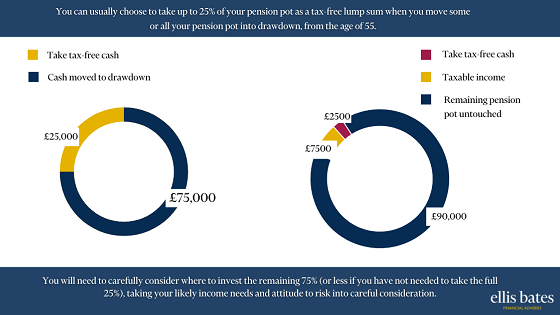

Flexi-access drawdown

https://www.ellisbates.com/wp-content/themes/osmosis/images/empty/thumbnail.jpg 150 150 Jess Easby Jess Easby https://secure.gravatar.com/avatar/70f816837c455030814d46a740cfc12d89893aaf8cbf8c8f8f59387d7b30ac08?s=96&d=mm&r=gFinancial Adviser, Andy King, discusses flexi-access drawdown.

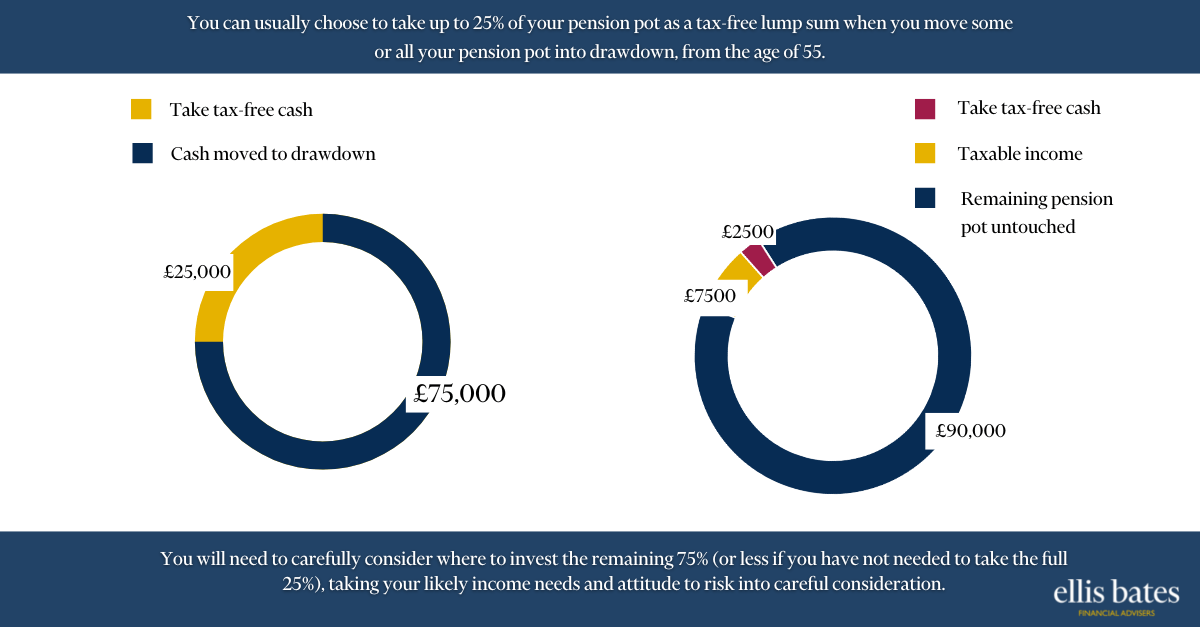

Flexi-access drawdown is one of the pension fund options at retirement and can also be referred to as flexible retirement income, or flexible income drawdown.

Choosing the best way to use your pension fund is complicated so it is important to seek professional financial advice to help you understand your options and to make the best decisions for your hard earned pension pot.