Wills & Probate

Rules of Intestacy

https://www.ellisbates.com/wp-content/themes/osmosis/images/empty/thumbnail.jpg 150 150 Jess Easby Jess Easby https://secure.gravatar.com/avatar/0e2a278e0eef1defdd7ee9d0ae7bb398?s=96&d=mm&r=gOur Estate Planning Specialist, Michelle Barker, discusses intestacy and the rules around intestacy including:

- What happens if you die without a Will

- Intestacy rules

- Examples of cases to show how the rules apply in England and Wales

- Intestacy in Scotland

- How to find out if someone has left a valid UK Will

Leaving your legacy behind

https://www.ellisbates.com/wp-content/uploads/2022/07/Leaving-your-legacy-behind.jpg 560 315 Jess Easby Jess Easby https://secure.gravatar.com/avatar/0e2a278e0eef1defdd7ee9d0ae7bb398?s=96&d=mm&r=gConsiderations when making a Will

Thinking about death isn’t easy. Talking about it is even harder. The reality of our own mortality is a tough subject, but a discussion will ensure your assets are left to the right people.

If you want to be sure your wishes are met after you die, then it’s important to have a Will. A Will is the only way to make sure your money and possessions that form your estate go to the people and causes you care about.

Unmarried partners, including same-sex couples who don’t have a registered civil partnership, have no right to inherit if there is no Will. One of the main reasons also for drawing up a Will is to mitigate a potential Inheritance Tax liability.

Statutory rules

Where a person dies without making a Will, the distribution of their estate becomes subject to the statutory rules of intestacy (where the person resides also determines how their property is distributed upon their death, which includes any bank accounts, securities, property and other assets they own at the time of death), which can lead to some unexpected and unfortunate consequences.

The beneficiaries of the deceased person that they want to benefit from their estate may be disinherited or left with a substantially smaller proportion of the estate than intended. Making a Will is the only way for an individual to indicate whom they want to benefit from their estate. Failure to take action could compromise the long-term financial security of the family.

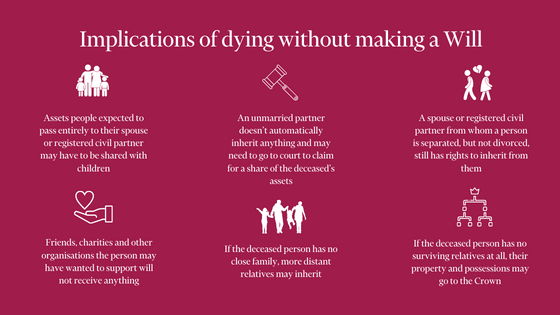

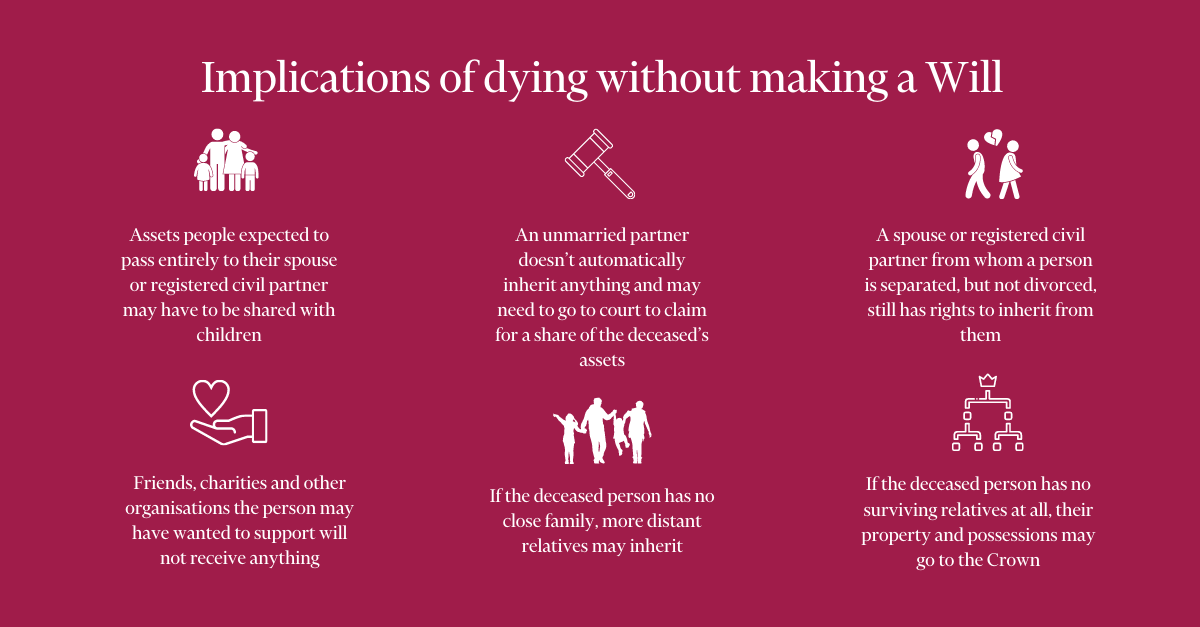

Implications of dying without making a Will

- Assets people expected to pass entirely to their spouse or registered civil partner may have to be shared with children

- An unmarried partner doesn’t automatically inherit anything and may need to go to court to claim for a share of the deceased’s assets

- A spouse or registered civil partner from whom a person is separated, but not divorced, still has rights to inherit from them

- Friends, charities and other organisations the person may have wanted to support will not receive anything

- If the deceased person has no close family, more distant relatives may inherit

- If the deceased person has no surviving relatives at all, their property and possessions may go to the Crown

Legal responsibility

Without a Will, relatives who inherit under the law will usually be expected to be the executors (someone named in a Will, or appointed by the court, who is given the legal responsibility to take care of a deceased person’s remaining financial obligations) of your estate. They might not be the best people to perform this role. Making a Will lets the person decide the people who should take on this task.

Where a Will has been made, it’s important to review it regularly to take account of changing circumstances. Unmarried partners have no right to inherit under the intestacy rules, nor do step-children who haven’t been legally adopted by their step-parent. Given today’s complicated and hanging family arrangements, Wills are often the only means of ensuring legacies for children of earlier relationships.

Simplifying the distribution of estates for a surviving spouse or registered civil partner

Changes to the intestacy rules covering England and Wales, which became effective on 1 October 2014, were aimed at simplifying the distribution of an estate and could mean a surviving spouse or registered civil partner receives a larger inheritance than under the previous rules.

Making a Will is also the cornerstone for Inheritance Tax and estate planning.

Before making a Will, a person needs to consider:

- Who will carry out the instructions in the Will (the executor/s)

- Nominating guardians to look after children if the person dies before they are aged 18

- Making sure people the person cares about are provided for

- What gifts are to be left for family and friends, and deciding how much they should receive

- What provision should be taken to minimise any Inheritance Tax that might be due on the person’s death

Preparing a Will

Before preparing a Will, a person needs to think about what possessions they are likely to have when they die, including properties, money, investments and even animals. Prior to an estate being distributed among beneficiaries, all debts and the funeral expenses must be paid. When a person has a joint bank account, the money passes automatically to the other account holder, and they can’t leave it to someone else.

Estate assets may include:

- A home and any other properties owned

- Savings in bank and building society accounts

- Insurance, such as life assurance or an endowment policy

- Pension funds that include a lump sum payment on death

- National Savings, such as Premium Bonds

- Investments such as stocks and shares, investment trusts, Individual Savings Accounts

- Motor vehicles

- Jewellery, antiques and other personal belongings

- Furniture and household contents

Liabilities may include:

- Mortgage(s)

- Credit card balance(s)

- Bank overdraft(s)

- Loan(s)

- Equity release

Jointly owned property and possessions

Arranging to own property and other assets jointly can be a way of protecting a person’s spouse or registered civil partner. For example, if someone has a joint bank account, their partner will continue to have access to the money they need for day-to-day living without having to wait for their affairs to be sorted out.

There are two ways that a person can own something jointly with someone else:

As tenants in common (called ‘common owners’ in Scotland)

Each person has their own distinct shares of the asset, which do not have to be equal. They can say in their Will who will inherit their share.

As joint tenants (called ‘joint owners’ in Scotland)

Individuals jointly own the asset so, if they die, the remaining owner(s) automatically inherits their share. A person cannot use their Will to leave their share to someone else.

Partial intestacy

This can sometimes happen even when there is a Will, for example, when the Will is not valid, or when it is valid but the beneficiaries

die before the testator (the person making the Will). Intestacy can also arise when there is a valid Will but some of the testator’s (person

who has made a Will or given a legacy) assets were not disposed of by the Will. This is called a ‘partial intestacy’. Intestacy therefore arises in all cases where a deceased person has failed to dispose of some or all of his or her assets by Will, hence the need to review a Will when events change.

Estate Protection

https://www.ellisbates.com/wp-content/uploads/2020/01/Estate-Protection.jpg 560 315 Jess Easby Jess Easby https://secure.gravatar.com/avatar/0e2a278e0eef1defdd7ee9d0ae7bb398?s=96&d=mm&r=g Preserving your wealth and transferring it effectively.

Preserving your wealth and transferring it effectively.

Estate planning is an important part of wealth management, no matter how much wealth you have built up. It’s the process of making a plan for how your assets will be distributed upon your death or incapacitation.

As a nation, we are reluctant to talk about inheritance. Through estate planning, however, you can ensure your assets are given to the people and organisations you care about, and you can also take steps to minimise the impact of taxes and other costs on your estate.

In order to establish the value of your estate, it is first necessary to calculate the total worth of all your assets. No matter how large or how modest, your estate is comprised of everything you own, including your home, cars, other properties, savings and investments, life insurance (if not written in an appropriate trust), furniture, jewellery, works of art, and any other personal possessions.

Having an effective estate plan in place will not only help to ensure that those you care about the most will be taken care of when you’re no longer around, but it can also help minimise Inheritance Tax (IHT) liabilities and ensure that assets are transferred in an orderly manner.

Write a Will

The reason to make a Will is to control how your estate is divided – but it isn’t just about money. Your Will is also the document in which you appoint guardians to look after your children or your dependents. Almost half (44%) of over-55s have not made a Will[1], and as such, they will not have any say in what happens to their assets when they die.

Should you die without a valid Will, you will have died intestate. In these cases, your assets are distributed according to the Intestacy Rules in a set order laid down by law. This order may not reflect your wishes.

Even for those who are married or in a registered civil partnership, dying without leaving a Will may mean that your spouse or registered civil partner does not inherit the whole of your estate. Remember: life and circumstances change over time, and your Will should reflect those changes – so keep it updated.

Make a Lasting Power of Attorney

Increasingly, more people in the UK are using legal instruments that ensure their affairs are looked after when they become incapable of looking after their finances or making decisions about their health and welfare.

By arranging a Lasting Power of Attorney, you are officially naming someone to have the power to take care of your property, your financial affairs, and your health and welfare if you suffer an incapacitating illness or injury.

Plan for Inheritance Tax

IHT is calculated based on the value of the property, money and possessions of someone who has died if the total value of their assets exceeds £325,000, or £650,000 if they’re married or widowed. If you plan ahead, it is usually possible to pass on more of your wealth to your chosen beneficiaries and to pay less IHT.

Since April 2017, an additional main residence nil-rate band allowance was phased in. It is currently worth £150,000, but it will rise to £175,000 per person by April this year. However, not everyone will be able to benefit from the new allowance, as you can only use it if you are passing your home to your children, grandchildren or any other lineal descendant. If you don’t have any direct descendants, you won’t qualify for the allowance.

The headline rate of IHT is 40%, though there are various exemptions, allowances and reliefs that mean that the effective rate paid on estates is usually lower. Those leaving some of their estate to registered charities can qualify for a reduced headline rate of 36% on the part of the estate they leave to family and friends.

Gift Assets while you’re Alive

One thing that’s important to remember when developing an estate plan is that the process isn’t just about passing on your assets when you die. It’s also about analysing your finances now and potentially making the most of your assets while you are still alive. By gifting assets to younger generations while you’re still around, you could enjoy seeing the assets put to good use, while simultaneously reducing your IHT bill.

Make use of Gift Allowances

One way to pass on wealth tax-efficiently is to take advantage of gift allowances that are in place. Every person is allowed to make an IHT-free gift of up to £3,000 in any tax year, and this allowance can be carried forward one year if you don’t use up all your allowance.

This means you and your partner could gift your children or grandchildren £6,000 this year (or £12,000 if your previous year’s allowances weren’t used up) and that gift won’t incur IHT. You can continue to make this gift annually.

You are able to make small gifts of up to £250 per year to anyone you like. There is no limit to the number of recipients in one tax year, and these small gifts will also be IHT-free provided you have made no other gifts to that person during the tax year.

A Potentially Exempt Transfer (PET) enables you to make gifts of unlimited value which will become exempt from Inheritance Tax if you survive for a period of seven years.

Gifts that are made out of surplus income can also be free of IHT, as long as detailed records are maintained.

IHT-Exempt Assets

There are a number of specialist asset classes that are exempt to IHT. Several of these exemptions stem from government efforts over the years to protect farms and businesses from large Inheritance Tax bills that could result in assets having to be sold off when they were passed down to the next generation. Business relief (BR) acts to protect business owners from IHT on their business assets. It extends to include the ownership of shares in any unlisted company. It also offers partial relief for those who own majority rights in listed companies, land, buildings or business machinery, or have such assets held in a trust.

Life Insurance within a Trust

A life insurance policy in trust is a legal arrangement that keeps a life insurance pay-out separate from the valuation of your estate after you die. By ring-fencing the proceeds from a life insurance policy by putting it in an appropriate trust, you could protect it from IHT. The proceeds of a trust are typically overseen by a trustee(s) whom you appoint. These proceeds go to the people you’ve chosen, known as your ‘beneficiaries’. It’s the responsibility of the trustee(s) to make sure the money you’ve set aside goes to whom you want it to after you pass away.

Keep Wealth within a Pension

When you die, your pension funds may be inherited by your loved ones. But who inherits, and how much, is governed by complex rules. Money left in your pensions can be passed on to anyone you choose more tax-efficiently than ever, depending on the type of pension you have, by you nominating to whom you would like to leave your pension savings (your Will won’t do this for you) and your age when you die, before or after the age of 75.

Your pension is normally free of IHT, unlike many other investments. It is not part of your taxable estate. Keeping your pension wealth within your pension fund and passing it down to future generations can be very tax-efficient estate planning.

It combines IHT-free investment returns and potentially, for some beneficiaries, tax-free withdrawals. Remember that any money you take out of your pension becomes part of your estate and could be subject to IHT. This includes any of your tax-free cash allowance which you might not have spent. Also, older style pensions may be inside your estate for IHT.

Make Sure Wealth Stays in the Right Hands

Estate planning is a complex area that is subject to regular regulatory change. Whatever you wish for your wealth, we can tailor a plan that reflects your priorities and particular circumstances. To find out more, or if you have any questions relating to estate planning, don’t hesitate to contact us.

Source data: [1] Brewin Dolphin research: Opinium surveyed 5,000 UK adults online between 30 August and 5 September 2018.

Information is based on our current understanding of taxation legislation and regulations. Any levels and bases of, and reliefs from. Taxation are subject to change. The rules around trusts are complicated, so you should always obtain professional advice. The value of investments and the income they produce can fall as well as rise. You may get back less than you invested.

Why Silence Isn’t Necessarily Bliss

https://www.ellisbates.com/wp-content/uploads/2019/12/Why-silence-isnt-necessarily-bliss.jpg 560 315 Jess Easby Jess Easby https://secure.gravatar.com/avatar/0e2a278e0eef1defdd7ee9d0ae7bb398?s=96&d=mm&r=g Over six million adults refuse to discuss their will with loved ones. Making a Will is very important if you care what happens to your money and your belongings after you die, and most of us do. But have you tried to talk with your children about your Will? If that conversation isn’t happening, you’re not alone.

Over six million adults refuse to discuss their will with loved ones. Making a Will is very important if you care what happens to your money and your belongings after you die, and most of us do. But have you tried to talk with your children about your Will? If that conversation isn’t happening, you’re not alone.

And it’s not only parents who are uncomfortable. Adult children may also be nervous about raising the topic of their parents’ finances for fear they appear greedy or nosy. Understandably, talking about dying can be seen as ‘taboo’ and it is not always easy to bring it up. However, discussing your Will with beneficiaries means they are better prepared when the time comes. However, worryingly, almost six and half million adults refuse to discuss their Will with loved ones according to new research[1]. A quarter (26%) of people with a Will say they will not discuss it as they do not want to think about dying, and one in four (27%) do not want to upset beneficiaries by discussing the contents of their Will[2]. It is also hugely important for family members to be aware of vital decisions in your Will, such as who will look after your children. By overcoming ‘death anxiety,’ the natural fear of talking about death and the emotions associated with it, these important conversations can ensure your beneficiaries are aware of your wishes and understand them. Nearly half (45%) of UK parents, the research identified, with adult children believe their Will is ‘no one’s business’ but their own or a partner’s. But sharing the contents of a Will makes the financial and practical consequences of death easier for those left behind. Losing someone can have a huge impact on finances for months or even years to come, so it is crucial for families to be prepared.

‘When I’m gone’ conversation with your partner or family

Avoid talking to someone when they’re busy. Look for opportunities to broach the subject, such as when you’re discussing the future or perhaps following the death of someone close to you

- Consider beginning the conversation with a question such as, ‘Have you ever wondered what would happen…?’; ‘Do you think we should talk about…?’

- Think about how you would manage financially should the worst happen. What impact would losing a partner or family member have on your household income and your expenses? Be aware that your financial situation may change in the future

- Make sure you know where all important documents such as Wills, bank details, insurance policies, etc. are kept, so that you have all the information you might need

- Prepare in advance – would you know how to manage the day-to-day finances? If not, consider how you could start to learn about them now so this doesn’t come as a shock

In the event of an illness, loss of capacity or death – are your plans in place?

Many of us will eventually reach a point in our lives when we require specialist assistance to ensure that our family will be able to cope better and manage their affairs in the event of an illness, loss of capacity or death. If you would like to review your particular situation, contact us to arrange an appointment.

Source data: [1] Royal London – six million figure is based on ONS adult population stats of 52.8million. Our research shows 47% of UK adults have a Will – 26% of this figure equates to 6,458,535.05 [2] Opinium on behalf of Royal London surveyed 2,006 adults between 26 and 29 October 2018. The survey was carried out online. The figures have been weighted and are representative of all GB adults (aged 18+).